In our country, the legal figure of the controlling beneficiary obeys the need to comply with international commitments with the Financial Action Task Force (FATF), to combat complex transactions and operations that allow the use of money of illicit origin and thus ensure the transparency of the beneficial owners of legal entities. Therefore, we will analyze the obligation to keep available the information of the controlling beneficiaries by the companies, that is, the natural persons behind a legal entity or structure.

It is important to emphasize that the idea that all beneficial owners engage in bad practices should not be generalized. Although the information is requested from all taxpayers, this is to allow the tax authority to strengthen its risk analysis and focus its audit powers on those taxpayers that really pose a risk and avoid imposing infractions.

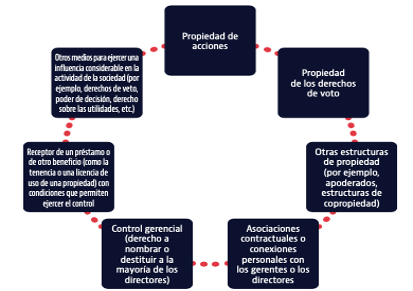

Examples of direct and indirect ownership and control:

Source: Manuel on final beneficiaries.

Now, in the explanatory memorandum of the tax reform of 2022, effective as of January 1, it is noted that the measures taken are for the purpose of facilitating the access of the tax authorities to accurate and updated information on the beneficial owners of individuals and legal structures, introducing in the CFF Articles 32-B Ter, 32-B Quáter, 32-B Quinquies, 84-M and 84-N, all of the Federal Tax Code, in correlation with the general rules to be published in the Miscellaneous Tax Resolution, which together establish the obligations and the way to comply with them, as well as the different assumptions of violations and penalties for noncompliance.

What should we understand by controlling beneficiary?

The controlling beneficiary is defined in Article 32-B Quáter of the CFF as the individual or group of individuals who directly or through another or others, obtains the benefit derived from their participation in a legal entity, a trust or any other legal entity, as well as from any other legal act, or is the person or persons who ultimately exercise the rights of use, enjoyment, use or disposition of a good or service or on whose behalf a transaction is carried out, even if they do it or do it on a contingent basis.

Likewise, the controlling beneficiary is the individual or group of individuals who directly, indirectly or contingently exercises control over the legal entity, trust or any other legal entity.

How to determine who is the controlling beneficiary?

The controlling beneficiary is the person or persons who effectively own or control or who benefit from the legal entity. According to the content of the 32-B Quárter, section II of the CFF, it can be seen that the legislator established when a natural person or group of natural persons exercises control when, through the ownership of securities, by contract or by any other legal act, it can or may successively exercise the following powers:

Who will be the obligated parties to provide information regarding the controlling beneficiary?

The regulated entities shall be the legal persons and legal entities obliged to identify, obtain, update, declare, keep and provide information on the controlling beneficiaries, including the supporting documentation. The following may be required about the controlling beneficiary:

Likewise, the Federal Fiscal Code indicates the following as obligated third parties with respect to the information of the controlling beneficiary:

What are the obligations of the regulated entities?

The obligations of the regulated entities are as follows:

What is the procedure for requesting information on controlling beneficiaries?

The SAT, upon request of requirement, which must be notified by tax mailbox, personally or by certified mail, the information of the controlling beneficiaries, through the following procedure:

Identification of beneficiary in legal entities:

What are the criteria for identifying the documentation to be provided related to the controlling beneficiary?

The maintenance of records by the regulated entities must be in an appropriate form and must be provided to the tax authorities and must include, among others, the following: full names and document with which the identity has been accredited, date of birth, sex, country of origin and nationality, CURP or its equivalent, country of residence, RFC code or its equivalent, marital status, contact information, home and tax address, description and form of participation, degree of participation, number of shares and partnership interests, date on which the individual acquired the status of controlling beneficiary, among others.

The foregoing is contemplated in rules 2.8.1.21 and 2.8.1.22 of the Miscellaneous Tax Resolution for 2023, where it is stipulated in its context that the obligated entities "shall implement internal control procedures duly documented. These procedures shall be all those that are reasonable and necessary to obtain and keep the information on the identification of the controlling beneficiaries and shall be considered part of the accounting that the SAT may require", in addition to specifying which is the information that the information must contain regarding each controlling beneficiary.

Will the authority be able to initiate verification powers for failure to provide the requested documentation?

Pursuant to Article 42, Sections XII and XIII of the CFF, in order to verify that financial institutions, fiduciaries, settlors or trustees, in the case of trusts; the contracting parties or members, in the case of any other legal entity; as well as third parties, comply with the provisions of Articles 32-B, Section V, 32-B Bis, 32-B Ter, 32-B Quáter and 32-B Quinquies of the CFF; the tax authorities are empowered to initiate the following verification powers:

What are the offenses committed by obligated entities that do not comply with the obligations established in articles 32-B Ter, 32-B Quárter and 32-B Quinquies of the CFF?

From the explanatory memorandum to the tax reform of 2022, it can be seen that the legislator considered providing for dissuasive sanctions for non-compliance with the obligations regarding the controlling beneficiary and added articles 84-M and 84-N of the CFF.

Derived from the above, persons who do not keep, do not obtain, or do not present the information referred to in articles 32-B Ter to 32-B Quinquies of the CFF, will be placed in the hypothesis of the infractions contemplated in articles 84-M and 84-N of the CFF, which range from 500,000 thousand to 2'000,000.00.

What is the period for which such information must be retained?

It was not identified in the legal provisions that regulate the beneficial owner that there is a term for the competent authorities to safeguard the information related to this figure; however, in a supplementary manner, the term of five years contemplated in Article 30 of the Federal Fiscal Code is considered.

In my opinion, although it is noted that the introduction of the legal figure of the controlling beneficiary complies with international standards, it is important to point out that it is the first step of many and it is noted that the regulation contained in the Federal Fiscal Code contains various uncertainties that cause uncertainty, so it is important that these measures should not infringe on the rights of taxpayers.

List of references.

Federal Fiscal Code. Last amendment DOF 12-11-2021. https://www.diputados.gob.mx/LeyesBiblio/pdf/CFF.pdf

Gaceta Parlamentaria, number 5864-D, dated September 08, 2021, Exposición de motivos de la reforma fiscal 2022. https://gaceta.diputados.gob.mx/PDF/65/2021/sep/20210908-D.pdf

Handbook on Beneficial Ownership. OECD. Secretariat of the Global Forum on Transparency and Exchange of Information for Tax Purposes. Inter-American Development Bank, March 2019.

https://www.dian.gov.co/Documents/Intercambio_de_Informacion_Internacional/Manual_sobre_beneficiario_efectivo_final_o_real.pdf

Controlling Beneficiary in the Mexican Tax System: Legal Effects and Reachability. PRODECON. Plascencia, Gómez, Balderas, Trejo, May 2022.

https://www.prodecon.gob.mx/Documentos/bannerPrincipal/2022/Beneficiario%20Controlador%20DIGITAL%20(1).pdf